The Memory Supercycle Has Reached Your MacBook

Welcome to Issue 56 of The Long Term Edge, your weekly guide to compounding over 7 or more years. This week the AI trade showed an effect on the supplier and customer sides. On Wednesday, Micron reported what may be the most extraordinary quarterly result in semiconductor history, with a revenue and guidance beat that was not anticipated. On Thursday, Apple confirmed that same trade is now reaching the consumer, announcing price increases of up to $500 on MacBooks and iPads and wiping $265 billion in market value in a single session. And by Friday, OpenAI had signalled it may delay its IPO to 2027.

Market Overview

Supplier Vs Consumer

Monday opened with Big Tech under pressure as markets reopened after the Juneteenth holiday. Alphabet fell 5%, SpaceX declined for the third consecutive session after its post-IPO peak, and the broader large-cap technology complex sold off. The Dow gained 0.2% while the Nasdaq fell 1.3% and the S&P 500 dropped 0.4%. Iran-US peace talks in Switzerland reported “encouraging progress” with both sides agreeing to a roadmap for a final deal within sixty days, and Brent crude fell further towards $78 a barrel.

Tuesday extended the losses. Bank of America issued a note raising its rate hike probability, and Asian markets collapsed overnight, with South Korea’s Kospi triggering an intraday circuit breaker before closing down 5.8%, its worst single session in over two years. The semiconductor complex bore the brunt in both Seoul and New York. The VanEck Semiconductor ETF fell more than 5% for the week overall.

Wednesday was Micron’s day. After the close, Micron reported fiscal Q3 2026 results that defied almost every model on Wall Street. The stock rose 14.55% in after-hours to $1,199.52. During the session, Brent crude fell 4.33% to $73.74, its lowest level since before the Iran conflict began in February, and the 10-year Treasury yield fell below 4.5%.

Thursday was Apple’s day and a brutal one. Apple announced price increases of up to $500 on MacBooks and iPads, citing “unprecedented” memory cost pressures driven by AI data centre demand. Apple fell 6.12%, its worst single session since April 2025, wiping approximately $265 billion in market value. The move triggered broader technology selling, with the AI price hike narrative spreading to other consumer electronics names. May PCE also landed: headline 4.1% year-on-year, the highest since April 2023; core 3.4% year-on-year, slightly above the 3.3% forecast. Q1 GDP final estimate came in at 2.1%, revised up from 1.6%. Personal income rose a stronger-than-expected 0.7%.

Friday closed the week with OpenAI’s IPO delay report. The New York Times reported that OpenAI is leaning towards delaying its IPO to 2027, with CEO Sam Altman reportedly rejecting any valuation below $1 trillion and advisers citing SpaceX’s post-IPO volatility, from a peak of $225.64 to an intraday low of $147.11 in just three sessions, as evidence that market appetite for mega-cap AI listings is more limited than previously assumed. Chip stocks fell again.

For the week: S&P 500 down nearly 2%, Nasdaq down 4.6%, Dow up 0.6%.

Week Ahead

Monday June 29

ISM Manufacturing PMI for June drops at 10 a.m. ET. After weeks of inflation data and macro noise, this gives the first read on factory activity for the month in which the Iran ceasefire framework was signed and oil prices fell sharply. Nike reports after the close.

Tuesday June 30

JOLTS job openings for May land, the first labour market read of the week ahead of Thursday’s payrolls data. Constellation Brands and General Mills report, adding consumer staples context to the week. Eurozone CPI also drops, which will be watched for signs of whether the energy shock from the Iran conflict has spread beyond US borders and at what pace it is now easing.

Wednesday July 1

ADP private payrolls drop alongside the ISM Services PMI for June, the last major preview before Thursday’s NFP. Both will be read closely against Warsh’s hawkish dot plot from the June FOMC meeting. Any sign that the labour market is softening, or that services activity is decelerating, would complicate the case for the rate hike nine FOMC officials projected for later this year.

Thursday July 2

The June Employment Situation report drops at 8:30 a.m. ET. This is the most consequential data point of the week. The prior two months, April at 172,000 and May at 179,000 revised, both nearly doubled their respective consensus estimates. A third consecutive strong print would make the case for the Fed’s first rate hike since the current tightening cycle began almost inarguable, regardless of how far energy prices have fallen since the Iran ceasefire. Markets close early at 1 p.m. ET ahead of the Independence Day holiday.

Friday July 4

US markets are closed for Independence Day. Investors head into the long weekend with the first half of 2026 behind them and a jobs report, a contested Iran ceasefire, a hawkish Fed, and an extraordinary earnings season all in context simultaneously.

Micron’s Quarter That Rewrote the Memory Playbook

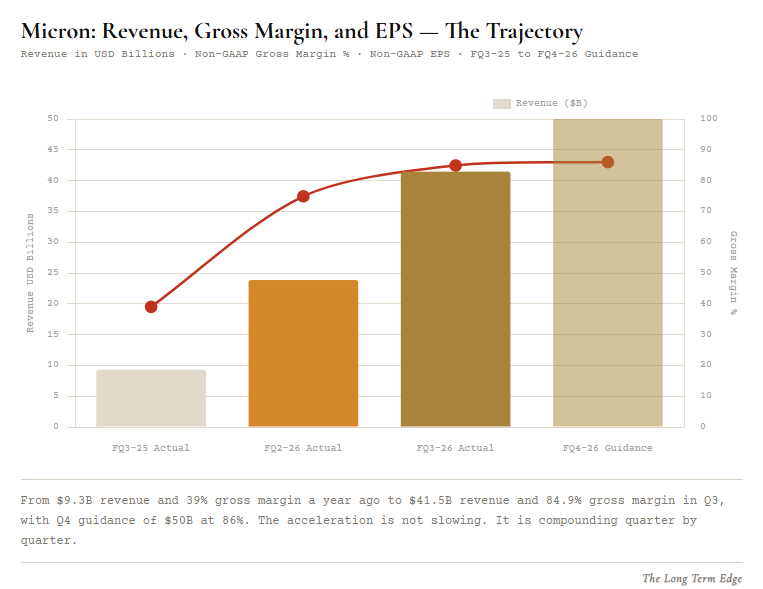

Revenue: $41.46 billion. Up from $23.86 billion in the prior quarter. Up from $9.30 billion a year ago. That is a 346% year-on-year increase in a single quarter for a company that was already the world’s third-largest memory manufacturer. Non-GAAP gross margin reached 84.9%, the highest in the company’s history. Operating income reached $33.68 billion on a non-GAAP basis, an operating margin of 81.2 per cent. Non-GAAP EPS of $25.11 beat the $20.49 consensus by 22.6%. Adjusted free cash flow reached $18.3 billion for the quarter alone. Cash on the balance sheet at quarter end stood at $24.99 billion, up from $9.64 billion just nine months earlier.

Q4 guidance of $50 billion in revenue with a gross margin of approximately 86% was more than double what most Wall Street models had projected for this time last year and meaningfully above the $43.58 billion consensus. If achieved, Micron’s fiscal full-year revenue will exceed approximately $170 billion, a figure that would make it one of the fastest top-line expansions in the history of the semiconductor industry.

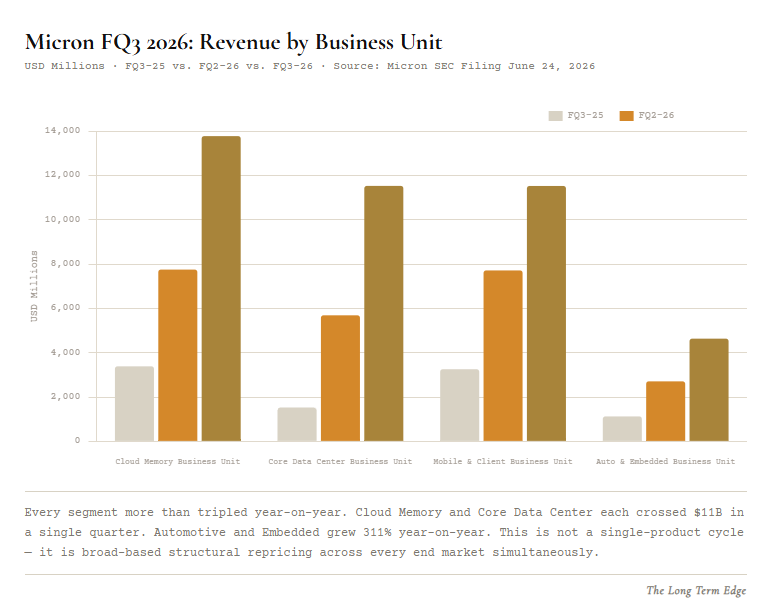

The segment breakdown is where the structural story lives. Cloud Memory Business Unit: revenue of $13.77 billion, gross margin of 83%, and operating margin of 78%. Core Data Center Business Unit: revenue of $11.52 billion, gross margin of 87%, and operating margin of 83%. Mobile and Client Business Unit: revenue of $11.52 billion, gross margin of 87%, operating margin of 86%. Automotive and Embedded: revenue of $4.63 billion, gross margin of 79%, operating margin of 75%. Every segment delivered operating margins above 75%. That is not a memory company in a cyclical upturn. That is a memory company that has structurally repriced its products across every customer category simultaneously.

The Strategic Customer Agreement disclosure is the detail that changes the long-term investment thesis most profoundly. Micron announced it has now signed sixteen SCAs with data centre operators, automakers, and other enterprise customers. For those SCAs with defined pricing, the company disclosed remaining performance obligations of approximately $100 billion at quarter end. Those obligations include binding commitments to purchase volumes of Micron’s chips over multi-year periods. The financial commitments from customers amount to $22 billion in deposits and advance payments. CEO Sanjay Mehrotra said on the call that when completed, he expects approximately half or more of the company’s revenue to be under these agreements. CFO Mark Murphy called it “transformational”.

The SCA structure is worth understanding in detail for long-term investors because it changes the fundamental risk profile of Micron as a business. The memory industry has historically been one of the most brutal in technology: hyper-cyclical, with periods of extraordinary profitability followed by periods of severe losses as supply caught up with and then exceeded demand. What the SCA structure does is remove a meaningful portion of that revenue from the spot market entirely. When half of Micron’s revenue is under multi-year, binding, volume-committed, fixed-or-floored-price agreements with hyperscalers and automakers, the quarterly swings that have historically defined this industry are removed. That is not a minor change. It is a business model transformation with direct implications for valuation, earnings predictability, and investor confidence in long-term forecasting.

HBM remains fully booked. Micron said tight supply conditions are expected to persist beyond calendar 2027. HBM4, built on 1-beta DRAM technology, is in high-volume shipments for the lead customer’s platform, with qualification samples shipped to multiple additional customers. HBM4E development, built on 1-gamma DRAM technology, is well underway, with volume production expected in calendar 2027. The progression from HBM4 to HBM4E, and the capacity commitments already secured for each generation, is the clearest available evidence that the structural demand cycle this newsletter identified has not peaked. It is still in its early expansion phase.

Apple’s Price Hikes and What They Confirm

On Thursday June 25, Apple raised prices on MacBooks, iPads, iMacs, HomePods, and Apple TV. The MacBook Air rose from $1,099 to $1,299. The MacBook Pro from $1,699 to $1,999. The iPad Air from $599 to $749. The Mac Studio with M3 Ultra jumped from $3,999 to $5,299, a 33% increase overnight. The average increase across affected products landed at approximately $246. The iPhone lineup was not touched. Apple’s stock fell 6.12%, its worst single session since April 2025, wiping approximately $265 billion of market value in a day. Microsoft raised Xbox console prices the same day, citing memory cost increases of more than 2.5 times and projecting another doubling by fall 2027.

Apple’s statement was explicit about the cause: “The rapid expansion of AI data centres has created an extraordinary surge in demand for memory and storage. We have never seen a component price increase this much, this quickly.” That framing, from the company that negotiates the largest consumer electronics memory contracts in the world, is not a complaint. It is a confirmation of the structural argument at the centre of this newsletter’s memory supercycle.

The iPhone exclusion is almost certainly temporary and strategic. IDC estimates that all new iPhone models moving to 12GB of RAM, required to support the full Apple Intelligence feature set, combined with the underlying DRAM cost increase, could add roughly $200 per unit to Apple’s bill of materials. Analysts at Counterpoint Research expect iPhone price increases of $150 to $200 across the lineup for the September iPhone 18 launch, weighted more heavily towards higher-memory configurations. IDC senior director Nabila Popal was unambiguous: “The iPhone isn’t spared; a price hike is coming. The storm isn’t over yet; this is just the beginning.” CEO Tim Cook will step back from the CEO role in September to become executive chairman, meaning the iPhone 18 pricing decision will likely be his last major product pricing call in the role.

Counterpoint Research director Tarun Pathak put the broader picture plainly: “Apple held it off for at least two quarters, protecting its user base from price inflation, but it has reached the point where it could no longer absorb the cost increase. We believe the situation is unlikely to improve for at least the next two years.” TrendForce data shows DRAM prices increasing up to 98% in the first quarter of 2026, with a further 58% to 63% increase expected in the current quarter.

For long-term investors, the Apple price hike announcement is significant for a reason that goes beyond Apple’s own stock price reaction. It is the clearest possible confirmation that the memory supercycle has crossed the boundary between AI infrastructure and consumer products. When the most powerful consumer hardware company in the world, with decades of supply chain leverage and the strongest supplier relationships in the industry, cannot absorb the cost increase and must pass it to customers, the companies on the supply side of that trade are in a structurally advantaged position. Micron reported the same week. The connection is not coincidental. It is causal.

For Apple itself, the long-term question is different. Price increases of this scale risk volume compression, particularly in markets outside the United States where Apple’s pricing is already at a premium to local alternatives. The MacBook Neo’s price increase specifically removes the one Apple product that was genuinely competitive on price with Windows and Chromebook alternatives. That is a strategic concession at the entry level that could have durable consequences for market share among younger, price-sensitive first-time buyers.

OpenAI Blinks. And Seoul Told You First.

By the time US markets opened on Tuesday, South Korea’s Kospi had already told the story. The index fell sharply enough intraday to trigger its circuit breaker mechanism, a decline that automatically halts trading to prevent panic selling, before closing down 5.8%. The dominant drivers: Samsung and SK Hynix, the two largest memory semiconductor companies in the world after Micron, sold off hard as the market reconsidered AI infrastructure valuations in the context of Apple’s anticipated price hike announcement and broader technology multiple compression.

This is worth understanding as a structural feature of how the memory and AI semiconductor trade works, not just as a one-week anecdote. South Korea’s stock market opens at 9 a.m. Seoul time, which is 8 p.m. the prior evening in New York. That means Korean market participants are digesting overnight US news, after-hours earnings releases, and early morning data before NYSE opens the following morning. For investors in Micron, Nvidia, AMD, or any company with significant exposure to the same semiconductor supply chain that runs through Samsung and SK Hynix, the Kospi and the performance of its major technology constituents can function as a leading indicator of how those names will trade when US markets open hours later.

In practical terms: when SK Hynix is down 7% in Seoul at midnight New York time, the probability that Micron opens lower in New York is meaningfully higher than it would otherwise be. When Samsung reports unexpected margin pressure, it tells you something about pricing dynamics that will eventually show up in Micron’s next quarter. The Korean market is not a perfect predictor, and there are company-specific factors that create divergence, but as a directional guide to the overnight sentiment shift in the AI memory trade, Seoul has earned attention from any long-term investor with exposure to the space. Monitoring Korean equity markets before the NYSE open is one of the most underappreciated informational edges available to retail investors who know what they are looking for.

This week illustrated the dynamic in both directions. Tuesday’s Kospi collapse front-ran the US semiconductor selloff by a full trading day. By Wednesday, when Micron reported results that obliterated every estimate, the after-hours move in MU immediately signalled a reversal in the narrative. By Thursday, when Apple announced its price hikes and the market reacted with a broad technology selloff, Seoul again gave an early read on the direction of travel.

The OpenAI IPO delay, reported Thursday evening, added a separate but related layer to the capital markets story. According to the New York Times, OpenAI’s advisers presented Sam Altman with two options: delay to 2027 at a target valuation of approximately $1 trillion, or list sooner at a lower valuation. Altman reportedly rejected any reduction from the trillion-dollar target, making the 2027 path the more likely outcome. The trigger for the reconsideration: SpaceX’s post-IPO trajectory. SPCX debuted at $135, rallied to a peak of $225.64, and then fell to an intraday low of $147.11 in the three sessions that followed, a 34% peak-to-trough move in days. For OpenAI’s bankers, that volatility was a data point about retail and institutional appetite for mega-cap AI listings that carried direct implications for OpenAI’s own offering.

The delay, if it holds, has cascading implications. SoftBank, which has approximately $65 billion committed to OpenAI and whose stock fell 13% on the news, had been counting on OpenAI’s IPO as a monetisation event that would validate its AI investment thesis. Anthropic, which has also filed confidentially for a US listing, must now recalibrate its own timing in the context of a market that has shown it will price even the most anticipated AI IPO with more scepticism than the pre-listing hype suggested. And for the broader AI trade, an OpenAI delay removes one of the largest potential sources of new AI-focused equity supply from the market this year, which is not uniformly negative for existing public AI names but does raise questions about what the delay signals about private market confidence in near-term AI monetisation timelines.

For long-term investors, the OpenAI story and the Kospi circuit breaker are two versions of the same question: how much future growth is already priced in to the AI trade, and what happens when the capital formation pipeline shows signs of friction? The answer this week was not reassuring for short-term holders. But for investors with a seven-plus-year horizon, weeks like this one, when the Nasdaq falls 4.6% and Seoul triggers a circuit breaker and OpenAI blinks on its IPO timeline, are when the businesses underneath the headlines can be evaluated more clearly than during the euphoria that preceded them.

May PCE and the Inflation Peak Question

May PCE came in at 4.1% year-on-year on the headline, the highest reading since April 2023, with core PCE at 3.4%, the highest since October 2023 and slightly above the 3.3% forecast. The monthly headline reading of 0.4% was below the 0.5% expected, while the core monthly reading of 0.3% matched forecasts. Services inflation accelerated to 0.5% monthly from 0.3% in each of the two prior months, the most concerning detail in an otherwise mixed report. Personal income rose a stronger-than-expected 0.7%, personal spending rose 0.7%, and the personal saving rate edged up to 3%.

The headline number matters because of what it likely confirms: May was almost certainly the peak of this inflationary cycle, and not because the Fed has done anything to bring it down. The energy shock from the Iran conflict drove the overwhelming majority of the headline acceleration. Brent crude has now fallen to $73.74, below where it was before the conflict began in February. That drop in oil prices does not yet appear in May’s PCE data, which measures prices paid through the end of May. It will begin showing up in June’s and July’s readings. The broader case for May as a peak is credible but not guaranteed. If services inflation continues at this pace through June and July, even a sharp drop in headline energy-driven PCE may not be enough to bring core comfortably below 3% by year’s end.

Deutsche Bank now expects two rate hikes this year, bringing the federal funds rate to 4.1%, with cuts not beginning until 2028. That call, which would have seemed extreme three months ago, is now within the range of mainstream forecasts. Nine of eighteen FOMC members already project at least one hike in Warsh’s own dot plot. The June jobs report on Thursday this week will be the next decisive data point: a third consecutive strong print would make the case for the Fed’s first hike almost inarguable, regardless of what happens to headline energy prices from here.

For long-term investors, the inflation picture heading into the second half of 2026 is more nuanced than either the bears or the bulls are acknowledging. The energy shock is easing, and headline PCE will likely fall meaningfully if the Iran ceasefire holds. Core inflation is stickier, driven by services and shelter, and is not responding to lower oil prices in any meaningful way. The Fed’s credibility question, how long it tolerates core PCE above 3% before acting, is what determines whether the second half of 2026 looks like 2023’s soft landing or something more disruptive. Warsh’s inaugural dot plot made clear which direction his committee is leaning. Thursday’s jobs number will tell us how much ammunition they have to act on it.

Closing Thoughts

The Same Trade, Seen From Both Sides

This week illustrated that the AI memory supercycle is not a single-company story, or even a single-sector story. It is a structural force that is now showing up simultaneously in Micron’s income statement, Apple’s retail pricing, South Korea’s stock exchange, OpenAI’s IPO timeline, and the Federal Reserve’s inflation projections.

Micron’s numbers, drawn directly from its SEC filing, are among the most extraordinary in semiconductor history. But they are also the mirror image of Apple’s price hike announcement. The same supply constraint that produced $41.46 billion in Micron revenue and an 84.9% gross margin is the same supply constraint that forced Apple to raise MacBook prices by $200 overnight. Both stories are true. Both have long-term investment implications. And they point in opposite directions depending on which side of the memory trade you are sitting on.

The OpenAI IPO delay and the KOSPI circuit breaker are the capital markets’ expression of the same underlying question the technology sector has been asking since Broadcom’s guidance miss three weeks ago: how much of the AI growth story is already priced in, and what happens to valuations when the capital formation pipeline shows friction? This newsletter does not have a confident short-term answer to that question. What it does have is a clear long-term framework: the businesses with structural, contractually embedded positions in the AI supply chain, Micron’s SCAs being the clearest current example, are materially better positioned to compound through that uncertainty than those dependent on spot market dynamics or IPO timing.

The second half of 2026 opens with a jobs report on Thursday, a contested ceasefire, a hawkish Fed chair with a dot plot that leans towards hiking, and a technology sector that has just had one of its most volatile fortnights since April 2025. That is not a comfortable starting position. It is, however, exactly the kind of environment in which the difference between businesses that compound through uncertainty and those that merely ride momentum becomes most clearly visible. That distinction is what this newsletter is built to identify, one week at a time.

Clarity compounds. Stay long-term.

Disclaimer: This newsletter is for informational purposes only and is not financial advice. Always do your own research or consult a licensed advisor.