Bumpy Ride Ahead

Welcome to Issue 53 of The Long Term Edge, your weekly guide to compounding over 7 or more years. The nine-week winning streak ended this week with a sharp reality check. Broadcom delivered record results and fell 12%. CrowdStrike beat on everything and fell 11%. Micron, which crossed $1 trillion last week, shed 13% on Friday alone. And the May jobs report, which doubled consensus expectations, sent the Nasdaq to its worst session since April 2025. This is the market in its new phase: one where good news has become bad news, and the rules of the AI trade have changed.

Market Overview

Nine Weeks Ended.

The week opened with momentum. The S&P 500 rose 0.26% on Monday to 7,599.96 and the Nasdaq gained 0.42%. Tuesday pushed further, with the S&P 500 closing above 7,600 for the first time ever at 7,609.78, and the Dow hitting a fresh all-time high at 51,307.79. Alphabet weighed slightly after announcing an $85 billion AI infrastructure fundraise through new stock sales.

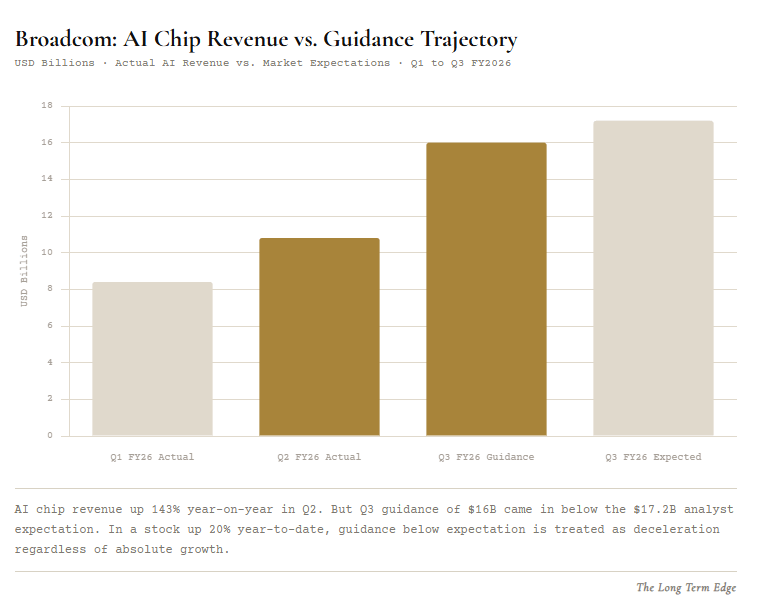

Wednesday was the pivot. Broadcom reported after the close: AI chip revenue of $10.8 billion, up 143% year-on-year. Total revenue of $22.19 billion, a record, up 48%. Adjusted EPS of $2.44, beating the $2.40 consensus. And yet the stock fell 12% in after-hours trading. The reasons: Broadcom left its full-year AI chip revenue forecast unchanged at $56 billion, and Q3 AI guidance of $16 billion came in below the $17.2 billion analysts had expected. CrowdStrike also reported Wednesday, beating on every metric including a 4-for-1 stock split announcement, and fell 11% in after-hours anyway.

Thursday spread the damage across the sector. Broadcom fell 12.6% on the session, dragging AMD and Intel down around 11%. The S&P 500 closed marginally higher only because non-tech sectors held. The Nasdaq ended fractionally lower. The VIX began climbing.

Friday delivered the week’s biggest shock. The May jobs report showed 172,000 positions added, nearly double the 85,000 consensus, with unemployment steady at 4.3%. The 10-year Treasury yield surged above 4.5%, and the 30-year crossed 5% for the first time in over a year. The Nasdaq fell 4.18%, its worst single session since April 2025. The S&P 500 dropped 2.64% to 7,383.74. The Dow lost 695 points. Semiconductor stocks bore the brunt: Marvell fell 16%, Micron 13%, AMD and Intel 11%, Nvidia nearly 6%. The VIX surged 34%, closing above 20 for the first time since April.

For the week: the S&P 500 fell more than 2%, the Nasdaq lost 4.7%. Nine consecutive weeks of gains. Over in one session.

Week Ahead

Monday, June 8

A quiet open. Campbell’s reports. Global manufacturing PMI readings give a read on industrial activity heading into what is a data-heavy week. Treasury markets will still be absorbing Friday’s yield surge, and any further movement in the 10-year or 30-year will set the tone for the session.

Tuesday, June 9

May existing home sales land, giving a read on whether elevated mortgage rates and inflation are cooling the housing market further. J.M. Smucker and Casey’s General Stores report, adding to the consumer picture. Bond markets will be the story, not equities, as traders position ahead of Wednesday’s CPI.

Wednesday, June 10

The most important data release of the week, and arguably of the summer. May CPI drops at 8:30 a.m. ET. Headline inflation is expected to come in at 4.2% year-on-year, up from 3.8% in April. That would be the highest headline CPI reading since early 2023. Core CPI is the critical number heading into the June 16 to 17 FOMC meeting. The trend is clear: March core was 2.6% and April core was 2.8%. If May continues that acceleration, the Fed’s first meeting under Kevin Warsh becomes the most consequential in the current cycle. Oracle reports after the close, providing a further read on enterprise cloud and AI infrastructure demand.

Thursday, June 11

May PPI drops alongside the ECB rate decision. The ECB is expected to hold rates, but its commentary on European inflation and energy costs will add a global dimension to the monetary policy picture. Adobe reports, giving a window into enterprise AI software adoption. Weekly jobless claims also land, the last labour market read before the FOMC meeting.

Friday, June 12

The preliminary University of Michigan consumer sentiment reading for June drops. After a week of inflation data, a surging VIX, and bond yields at multi-year highs, this will tell us whether the consumer is beginning to feel it. It is also the last major data release before the June 16 to 17 FOMC meeting. Whatever it shows, Kevin Warsh will be reading it alongside the CPI, PPI, and jobs prints when the committee convenes.

Broadcom and the New Rules of the AI Trade

Broadcom delivered one of the most impressive quarters in semiconductor history. AI chip revenue of $10.8 billion, up 143% year-on-year. Total revenue of $22.19 billion, a record, up 48%. Adjusted EPS of $2.44, beating estimates. Record free cash flow of $10.26 billion, representing 46% of revenue. The company ended the quarter with $19.6 billion in cash. By any conventional measure, it was an extraordinary result.

The stock fell 12% anyway.

Understanding why reveals something important about where the AI trade is now. Broadcom left its full-year 2026 AI chip revenue forecast unchanged at $56 billion. Its Q3 AI chip guidance of $16 billion came in below analyst expectations of $17.2 billion. CEO Hock Tan disclosed that Google would likely draw on multiple chip suppliers rather than Broadcom exclusively, raising questions about customer concentration risk. And Tan acknowledged that surging AI semiconductor sales were diluting the company’s overall gross margins as the product mix shifted.

None of these disclosures change the fundamental reality that Broadcom is one of the most important AI infrastructure companies in the world. It designs custom AI accelerators for some of the largest organisations on the planet, including Anthropic, Google, Meta, and OpenAI. Its networking chips are essential to every large-scale AI cluster. Its FY2027 AI chip revenue target of more than $100 billion, reiterated on the call, represents a business that does not yet exist at anything close to that scale in today’s market.

But the market had priced in something more. Broadcom shares were up over 20% year-to-date entering the session. The stock was trading at all-time highs. At that price, the bar for what constitutes a positive earnings event had moved well above what most companies could ever deliver. A 143% year-on-year increase in AI chip revenue was not enough, because the market had already decided that acceleration was the baseline. Holding the full-year forecast was read not as discipline but as a ceiling signal.

For long-term investors, Broadcom’s week illustrates the new rules of the AI trade with unusual clarity. In the first phase of the AI investment cycle, beating estimates was sufficient to send stocks higher. In the current phase, beating estimates is necessary but not sufficient. Guidance must also accelerate beyond what analysts have already modelled. When Broadcom said $16 billion for Q3 and analysts expected $17.2 billion, the interpretation was not that Q3 will still be extraordinary. The interpretation was that the acceleration story had a ceiling the market had not previously priced.

The 46 analysts who maintain a strong buy consensus on Broadcom with an average 12-month price target of $497.74 have not changed their fundamental view. The business remains exceptional. What changed this week is not the business. It is the expectations’ environment that surrounds it.

The Jobs Report That Changed Everything

The May jobs report showed 172,000 positions added. The consensus estimate was 85,000. April was revised up to 179,000. The unemployment rate held at 4.3% for the fourth consecutive month. By any conventional measure of labour market health, these are strong numbers.

The market’s response: the Nasdaq fell 4.18%, its worst session since April 2025. The 10-year Treasury yield surged above 4.5%. The 30-year crossed 5% for the first time in over a year. The VIX surged 34% to above 20.

This is good-news-is-bad-news at its most extreme. And the mechanism is straightforward: a labour market this strong, combined with core PCE at 3.3% and headline inflation expected to reach 4.2% in May, removes any remaining argument for rate cuts and puts rate hikes firmly back on the table heading into the June 16 to 17 FOMC meeting.

The report had one genuine note of complexity. Average hourly earnings rose just 3.4% year-on-year, the lowest since 2021. That is below inflation, meaning real wages remain negative. The labour market is adding jobs, but those jobs are not paying enough to outrun prices. For workers, that combination is straightforwardly bad. For the Fed, it is a partial complication: if wage growth is not accelerating, services inflation may not be as entrenched as the headline jobs number suggests. Goldman Sachs cited this nuance in its post-report note, saying the data increases the risk of a longer pause but does not make rate hikes a certainty.

Cleveland Fed President Beth Hammack was less equivocal. She said it may soon be appropriate for the Fed to act to address the growing risks of persistently elevated inflation. Morgan Stanley’s Ellen Zentner called the report strong from every angle and said the Fed remains watching and waiting, focused on the inflation side of its mandate. A watching and waiting Fed with a strong jobs market and accelerating inflation is a Fed that is running out of reasons to stay still.

The June 16 to 17 FOMC meeting will be Kevin Warsh’s first as chair. He will have May’s NFP, Wednesday’s CPI, Thursday’s PPI, and April’s core PCE all in hand. The data corridor between now and that meeting is the most consequential two-week stretch of the current cycle. History suggests that a new Fed chair can affect market trends, and that it may take a few meetings for investors to calibrate how hawkish or dovish Warsh’s language will be relative to Powell’s. Either way, the jobs report has made sure the first meeting matters.

May CPI Wednesday: The Number That Sets the Summer

Wednesday, June 10, is the most important single data release of the summer. May CPI drops at 8:30 a.m. ET, and what it shows will determine the tenor of the June 16 to 17 FOMC meeting, the trajectory of bond yields through July, and whether the equity market’s repricing this week is the beginning of a larger reset or a short-term buying opportunity.

Headline CPI is expected to come in at 4.2% year-on-year, up from 3.8% in April. If confirmed, that would be the highest headline reading since early 2023. The energy shock from the Iran conflict accounts for a significant portion of that acceleration. Gasoline prices have remained elevated through May, and the full pass-through of April’s oil price spike has not yet fully registered in monthly price data.

Core CPI is the number that matters most for the Fed. The trend over recent months has been consistent: March’s core was 2.6% and April’s core was 2.8%. If May prints at 3.0% or above, it would represent clear evidence that inflation is broadening beyond energy and into the structural categories; shelter, services, transportation, that the Fed finds most difficult to address through rate policy without inducing a recession.

The timing makes this print unusually consequential. The Fed does not meet again until June 16 to 17. The FOMC will have May CPI, May PPI, and April PCE all available when it sits down to deliberate. Warsh’s first meeting as chair will be shaped almost entirely by the data that arrives in the next seven days. If core CPI accelerates and PPI follows, the probability of a rate hike at that meeting or at the one that follows in late July becomes difficult to dismiss.

For long-term investors, the CPI print does not change the underlying business cases of the companies discussed in this issue. Broadcom’s custom AI chip business, CrowdStrike’s cybersecurity platform, Micron’s HBM manufacturing advantage — none of these are materially affected by whether core CPI prints at 2.8% or 3.1% on Wednesday. What does change is the discount rate that the market applies to future earnings, the cost of capital for companies financing growth, and the sentiment environment in which all of these businesses trade. In that sense, Wednesday’s number matters not because it changes the fundamentals, but because it determines how long investors are willing to wait for those fundamentals to be fully rewarded.

When Good News Becomes Bad News: CrowdStrike and Micron

CrowdStrike reported one of the strongest quarters in its history on Wednesday, June 3. Revenue of $1.39 billion, up 26% year-on-year, beating estimates. Adjusted EPS of $1.10 against a $1.07 forecast. Record net new ARR of $256 million, up 32%. Record free cash flow of $468 million. A raised full-year guidance. A 4-for-1 stock split announcement. GAAP net income turned positive for the first time at $27.8 million, compared to a loss of $104.3 million a year earlier.

By any conventional scorecard, it was a clean, dominant quarter. The stock fell 11% in after-hours trading.

Micron crossed $1 trillion in market capitalisation last Tuesday on a 19% single-session gain. By Friday, it had given back 13% of that in a single day, pulled down entirely by the macro selloff triggered by the jobs report. No company-specific news. No earnings miss. No guidance change. Just a strong jobs print pushing Treasury yields higher, which pushed technology valuations lower, which sent a stock that had risen 19% in a week down 13%.

Both stories illustrate the same underlying dynamic: the AI trade has entered a regime in which valuation is the determining variable, not quality. CrowdStrike’s shares were up nearly 65% year-to-date entering Wednesday’s session. The stock was trading at a forward price-to-earnings ratio of approximately 154 times. At that multiple, billing growth of 18%, below analyst expectations even as revenue grew 26%, was enough to trigger a re-rating. The market is not asking whether CrowdStrike is a great business. It is asking whether it is a great business at $747 per share. On Wednesday night, the answer was no.

Micron’s situation is different but related. The fundamental thesis is intact: HBM supply is sold out through 2026, AI GPU demand is compounding, and Micron is the only US-based manufacturer of advanced memory. None of that changed on Friday. What changed is that a strong jobs report pushed the 30-year Treasury yield above 5%, which mechanically increases the discount rate applied to future earnings, which reduces the present value of long-duration growth stocks. Micron, up nearly 850% over the prior 18 months, carries a significant amount of future growth in its price. When discount rates move, that future growth becomes less valuable in today’s terms.

For long-term investors, the lesson from both CrowdStrike and Micron this week is not that the AI trade is over. The businesses are excellent. The structural demand drivers are real. The lesson is about the difference between owning a great business and owning a great business at the right price. In a regime where good news becomes bad news, where record results send stocks down 11% and macro surprises compress valuations irrespective of fundamentals, the margin of safety in your entry price is the only variable fully within your control.

CrowdStrike’s 4-for-1 stock split, effective July 2, will increase retail accessibility and liquidity. The business case has not weakened. Micron’s HBM advantage has not narrowed. What has happened is that the market has used a week of external pressure to reprice both stocks towards a more rational relationship between price and expected future cash flows. Whether this week’s levels represent that rational relationship is the question worth sitting with before acting in either direction.

Closing Thoughts

What the Winning Streak Ending Actually Means

Nine consecutive weeks of gains ended on Friday with the Nasdaq’s worst session since April 2025. The VIX is above 20 for the first time since April. The 30-year Treasury yield is above 5%. Rate hike odds have moved from 45% to something that is no longer being dismissed as a tail risk.

It would be easy to frame this as a turning point. Markets reversed. The AI trade stumbled. The jobs data changed the calculus. But the more accurate framing is simpler: the market was pricing a set of assumptions that required a specific path for inflation, rates, and AI revenue acceleration. This week, all three of those assumptions were tested. Broadcom’s guidance held flat when the market needed it to accelerate. The jobs report removed the last argument for near-term rate cuts. And CrowdStrike’s billings growth disappointed even as revenue accelerated.

None of these are existential events for the companies involved or for the broader AI investment thesis. They are recalibrations. The market is adjusting its expectations towards something more consistent with the actual trajectory of the data. That process is uncomfortable when it happens quickly, but it is healthy over time. Valuations that outrun earnings growth eventually come back. When they do, the businesses underneath them are often better than they were when the premium was at its peak.

Wednesday’s CPI print will tell us whether this week’s repricing is the beginning of something larger or a sharp but contained reset. Either way, the long-term edge is not built by predicting which way that print lands. It is built by owning businesses that can compound through the uncertainty that surrounds it.

Clarity compounds. Stay long-term.

Disclaimer: This newsletter is for informational purposes only and is not financial advice. Always do your own research or consult a licensed advisor.